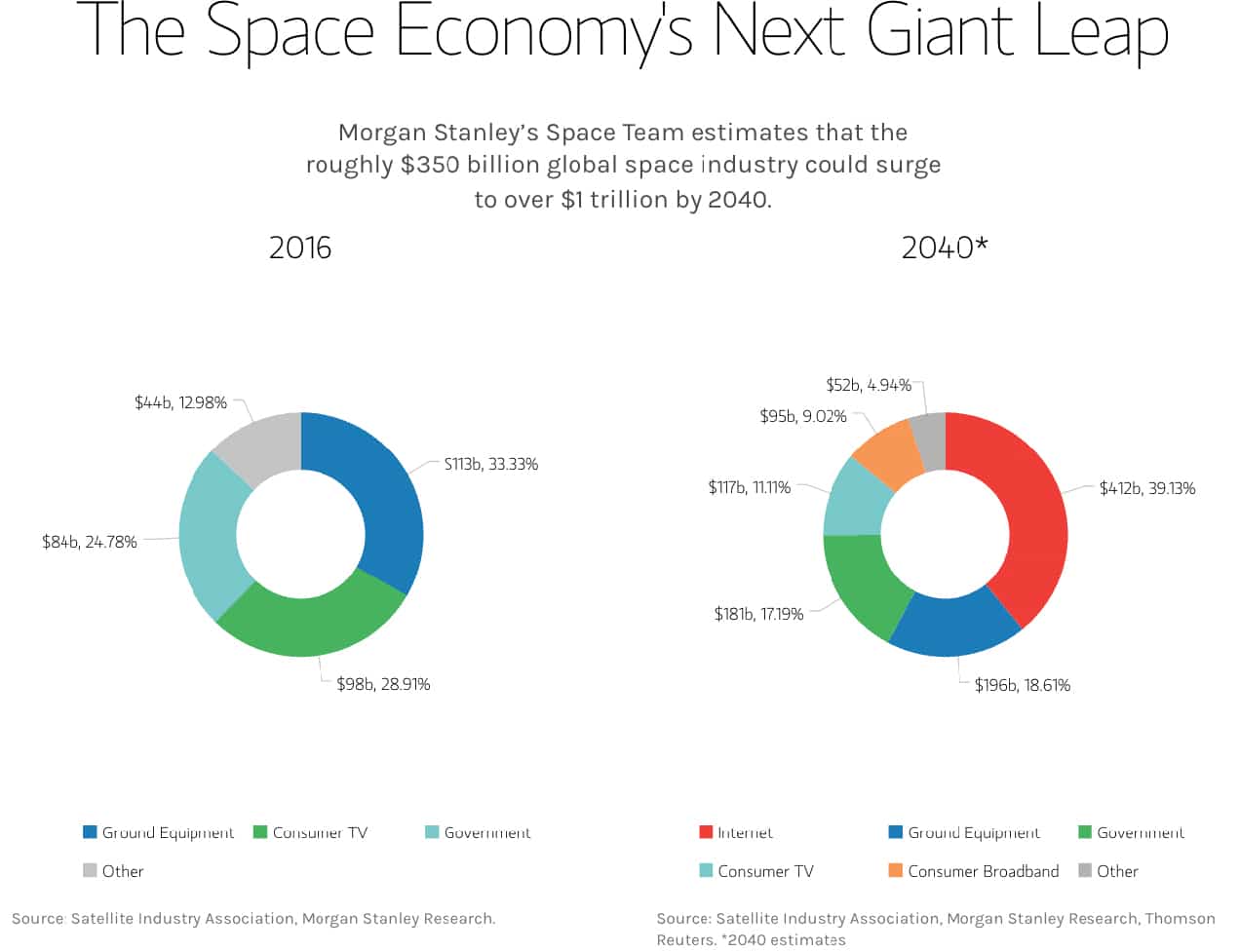

Hardly a day passes without an important and inspiring Space development, be it exploration of Mars, increased human spaceflight, improved communications, navigation, and analytic insights from Space-based assets here on Earth, and many others. As the global Space economy heads rapidly toward its first half-trillion dollars of value, with estimates of one to three trillion dollars by 2030, we need to understand the sources of innovation that will drive it and some of the new areas it will impact here, on our lives on Earth.

To be a bit more specific, last year the Space Foundation estimated that the size of the global Space economy in 2020 had grown at a rate of 4.4 percent to nearly USD 447 billion, with commercial activities representing nearly 80 percent of that total. While this growth rate may seem modest, it is important to remember that it took place during one of the largest economic contractions in history. A separate study by Euroconsult said that government investment in Space in 2021 hit a record USD 92 billion, and was dominated by Space exploration and military Space activities.

Space has an outsized impact on our daily lives, by some estimates adding over five trillion dollars in direct and indirect economic value in the United States alone, by enabling financial services, entertainment, weather prediction, navigation, communications, and many other sectors. Space has, for sure, played an important role in helping us mitigate the effects of the COVID-19 pandemic, be it by providing unique insights into macro-economic developments on Earth, allowing for remote monitoring of facilities and the precise delivery of goods and services, or through advancing necessary developments in telemedicine and distance education.

Geospatial observers are already well aware of one of the most important developments — leveraging the content derived from remote sensing data is already one of the fastest-growing segments of the Space economy. The lesson from remote sensing history that certainly applies to other Space market segments is that end-users want information, not raw data, which is focused on their own sectors like agriculture, insurance, or even national security. Remote sensing use began to grow quickly when firms applied artificial intelligence and other analytic techniques, and then focused on the applications in these specific market segments.

The contributions don’t stop there. The Space economy is accelerating and diversifying as a wide range of entrepreneurs, backed by government and private investment, bring new ideas into the market. We are moving quickly from a historically limited set of conversations about Space-based remote sensing, communications, and launch to a broader set of near-term market services like on-orbit manufacturing, Space tourism, Space medicine, and the exciting near-term development of a lunar economy. Entrepreneurs who want to provide new Space services can use the lower costs and increasing availability of launch to try out technical solutions, validate or adapt them, and quickly bring them to market. Demand is also changing: companies from a wide range of industrial sectors, but traditionally not involved in any way with Space, are now beginning to leverage Space capabilities, based on those same economic realities.

For one, many of the emerging Space market segments are broad and deep, meaning that there are multiple players pursuing ideas in similar market areas. One may be skeptical about the idea of a lunar economy, but with more than 90 missions planned by the end of the decade, it is almost certain that some of them, and perhaps most of them, will succeed. Aside from the scientific exploration missions that include assessing the quality of water ice on the Moon — a potential game changer for further solar system exploration — other missions will be designed to help develop the infrastructure for a permanent presence on the lunar surface.

Government investments in the Space economy remain vitally important but are changing, as public institutions like NASA and the US Department of Defense look to new acquisition strategies that involve initial investment rather than anchor tenancy. Meanwhile, an unprecedented level of private investment into the Space economy — over USD 46 billion in 2021 alone, and over USD 250 billion in the past decade — not only encourages diversity of business and technical approaches but helps create additional demand beyond traditional government demand.

In fact, innovations in the Space economy are converging from many different directions, so it is important to highlight some of them here. Briefly, five key areas that are driving innovation are:

While advances in the Space economy portend great achievements in the human exploration of outer Space and for improving our lives on Earth, there are important challenges. Not everyone who enters the market will succeed, although the Space economy now shifts toward a normal market where we will see winners and losers, mergers and acquisitions, consolidation, and many of the other behaviors we see in other markets.

The key will be understanding and adjusting to competition. There is intense competition brewing in the small satellite launch business, which today claims over 170 companies worldwide pursuing a wonderfully diverse set of business and technical approaches. It is inevitable that some consolidation will take place in the next few years.

The LEO (low earth orbit) satellite communications market may also be headed for consolidation and even commoditization. The number of communications satellites grew rapidly from 2200 at the beginning of 2021 to over 3000 by year end, mainly from SpaceX and OneWeb. Planned satellite deployments by these companies — as well as by Amazon Kuiper, Telesat Canada, and a Chinese system — over the next five years, will raise the numbers by thousands.

Just like the diversity in the launch business, the LEO communications business will see direct-to-consumer models, ones that will leverage traditional telecommunications companies, and yet others that will leverage Cloud-based connectivity. These competing delivery systems will use price as one competitive tool.

There’s also a key question of ultimate demand. Between three and four billion people on earth are estimated to be unserved or underserved in communications and internet access, and demand is still increasing in developed economies as new applications emerge. The key question is how many of these constellations will respond to actual market demand, and at what price points? This is another potential source of intense price competition.

We also cannot ignore the Chinese satellite communications constellation as an additional source of price competition and the introduction of anti-competitive behavior. China’s overall aims in Space, and its ‘belt and road’ initiative designed to lock up emerging Space partners, could negatively affect market size and fair competition in this arena.

Aside from strategic consequences, any conflict in Space could dampen investor and entrepreneur confidence and therefore the growth of commercial Space activities.

Security interests and the nature of strategic competition are changing. China’s recent white paper speaks to a “new stage of rapid development and profound transformation,” and posits developments in “Space exploration, Space transportation, the modernization of Space governance, and new forms of international cooperation.” Russia’s highly irresponsible destruction of one of its own satellites in November 2021, followed by explicit threats to the United States’ GPS constellation, reflects growing geopolitical competition that can extend to Space activities.

Aside from strategic consequences, any conflict in Space could dampen investor and entrepreneur confidence and therefore the growth of commercial Space activities. Moreover, traditional military Space competition, the growing importance of the Space economy brings strategic importance to issues like foreign investment, export controls, and economic competitiveness of the Space industry.

Finally, we need to deal with the urgent issues of Space debris and congestion. Remnants of rockets, dead satellites, and other bodies litter Space in every orbit, and threaten the lives on board the International Space Station, the billions of dollars of US and international investment in Space, and the growth of the Space economy. Solutions lie at the nexus of a very complex set of legal, technical, and international issues. First up is the need to improve our understanding of the Space environment in order to provide more timely warnings about possible collisions (also known as conjunctions) to Space operators.

Beyond that lies the opportunity and necessity for a much more diverse Space safety industry as fundamental to the growing Space economy. New tools to enhance Space situational awareness and active debris removal are entering the market, although the international political and legal frameworks to effectively use them are still lacking. Dealing with this challenge is an absolute necessity if we are going to realize the scientific and economic benefits of Space anticipated over the next decade and beyond.

© Geospatial Media and Communications. All Rights Reserved.